PPP Alternatives: What to Do If You’re Rejected for a PPP Loan

PPP Alternatives: What to Do If You’re Rejected for a PPP LoanFeeling frustrated after getting rejected for a PPP loan?

You’re not alone.

There are reasons why you might’ve been rejected for a PPP loan though, but don’t worry – there are many other funding options available.

The Paycheck Protection Program

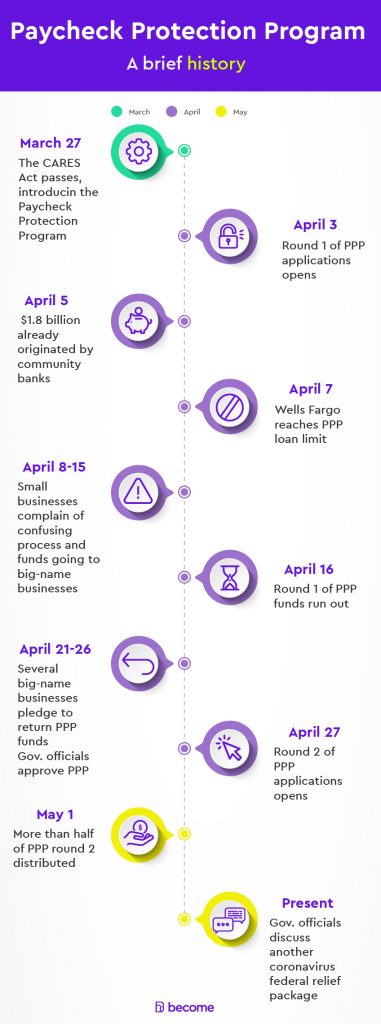

The Paycheck Protection Program was signed into law on March 27, 2020 under the CARES Act. Applications for that first round of small business emergency funding, totaling $349 billion, opened on April 3.

By April 5, smaller community banks had already originated more than $1.8 billion in PPP loans. This seemed to signal that the funds were going where they were most needed – in smaller communities to smaller businesses.

It wasn’t all good news though, as two days later, on April 7, Wells Fargo (one of the nation’s largest lenders) announced that it had reached its PPP loan limit. Thousands of business owners, already confused by the wobbly program, had to turn elsewhere to apply. Some simply gave up and began searching for PPP alternatives. Complaints quickly began circulating about how unclear and incomplete the program was both from business owners and lenders.

On April 16, a mere 13 days after PPP applications started, the SBA officially announced that funds had run out. Government officials had already been discussing a second round of PPP funding a week prior.

Before the official announcement, small businesses and economic watchdogs were crying foul over the fact that several big-name businesses were obtaining millions of dollars in relief loans that were meant for mom-and-pop businesses. Those larger businesses had exploited a loophole that allowed restaurants to get approved for PPP loans as long as they had fewer than 500 employees at any given location. And at the same time, some small businesses were even rejected for a PPP loan. Of course, this resulted in lots of frustrated business owners.

Between April 21 and April 26, as pressure was mounting for government officials to do something about that glaring fault in the program, some of those big businesses decided that it was in their best interest to return the funds they had received through PPP loans. Those businesses included Ruth’s Chris Steak House, Potbelly, and Shake Shack – along with a host of law firms and financial firms.

At the end of that week, some good news came as government officials approved a second round of PPP funds – amounting to $310 billion. Applications reopened on April 27.

By May 1, more than half of PPP 2.0 had been distributed – roughly $175.7 billion. Treasury Secretary Steven Mnuchin said that the average size of loans under PPP 2.0 was roughly $79,000 – compared to an average of roughly $200,000 in the first round. Once again, signaling that the loans are going where they should be.

The government then approved another round of Paycheck Protection Program funding.

Reasons for PPP loan rejection

There are a number of reasons why you may be rejected for a PPP loan. First and foremost, before you apply you needed to have checked that you had all of the required information and documentation on hand.

That will typically include:

- General business information (name/address/contact)

- Documents detailing your business’s legal structure/ownership

- Tax returns for 2019

- Proof of business activity

- Proof that your business has been directly impacted by coronavirus

- Utility expense reports

- Mortgage/rent statements

- Payroll reports

If any of the above information or documents were missing from your application, that could be why you were rejected. Additionally, the PPP application specified another five reasons why you may be declined PPP funding. Your Paycheck Protection Program eligibility may be declined if:

- You’re delinquent or have defaulted on any federally-guaranteed loans in the past 7 years

- You or any other owner of your business is suspended from Federal financial aid

- You or any other owner of your business is presently involved in any bankruptcy

- You or any other owner of your business is presently facing criminal charges or is on probation/parole

- You or any other owner of your business has been convicted of a felony in the past 5 years

What to do if your business was rejected for a PPP loan

Besides searching for PPP alternatives (we get to that below) there are some other steps you can take to keep your business up-and-running until you either get the federal aid you need, or until things return to normal.

Believe it or not, there are ways that you can increase your business’s cash flow during the coronavirus pandemic. Those ways include cutting costs, renegotiating deals with suppliers, asking your lender(s) to defer payments, selling off assets, taking your business online, and more.

Can you reapply for the Paycheck Protection Program?

The general rule with reapplying for the Paycheck Protection Program is that if you haven’t received a PPP loan, you may reapply. Just be sure that once you do get approved for a PPP loan, you cancel all other applications that you’ve previously submitted. Taking multiple PPP loans is forbidden.

Can you submit multiple applications through different PPP lenders?

The answer here is essentially the same as above. You may submit multiple applications through different PPP lenders as long as you only accept one PPP loan. And once you do receive the funds, you are advised to cancel all other applications you may have submitted elsewhere.

What if you don’t hear back from the SBA?

Technically, the SBA only becomes relevant once the lender or bank you applied through gets your application approved. When your application is approved you will need to stay in contact with your lender in order to finalize the process and receive your PPP loan. If you don’t hear back from your lender or bank, you may want to consider applying again through a different source.

Even if you’re set on getting approved for a PPP loan, you should still have a backup plan or two lined up if things don’t go as expected.

That’s where PPP alternatives come in…

5 PPP loan alternatives

For some small businesses, the Paycheck Protection Program just isn’t going to be the solution that gets them through this financial crisis. Fortunately, PPP alternatives exist, and plenty of them!

From other federal aid programs to those organized by state and local governments, to privately sponsored initiatives – the list of PPP alternatives is extensive, to say the least.

Here are 5 of the top PPP alternatives that your business can potentially make use of (see the full list):

1. Economic Injury Disaster Loan Program

The Economic Injury Disaster Loan program has been around for a while but has received some revisions thanks to the passing of the CARES Act. The loans provided through the EIDL program are designed to help businesses facing economic injury as a direct result of a disaster. This crisis is unprecedented in the sense that it is the first time that every state in the country has been designated a disaster zone all at once, meaning businesses in all states are potentially eligible for an EIDL.

The two main changes made to the EIDL are that interest rates have been reduced to 3.75% for businesses and, more notably, businesses can quickly receive up to $10,000 in the form of an advance on the loan – something that’s attracting the attention of many business owners these days.

2. SBA Express Bridge Loans

If your business has an existing relationship with an SBA Express Lender, then you may be able to obtain up to $25,000 in the form of a fast bridge loan. The SBA Express Bridge Loan Pilot Program is meant to fill the gap in a business’s revenue while they apply and wait for a response from the EIDL program. In fact, the bridge loan is repaid either in part or in full with the funds you ultimately receive through the EIDL program.

3. Facebook’s Small Business Grants Program

Do you have between 2 and 50 employees? Has your business been operating for at least a year? Then you may be eligible for a small business grant from Facebook that can help you meet operational costs, cover rent, and keep your employees on the payroll.

There is one catch: you need to be located in a fairly specific area, one that’s been designated by Facebook. Be sure to check the official Facebook Small Business Grants Program website and see if you’re based in an eligible location.

4. Amazon’s Neighborhood Small Business Relief Fund

The important note for this program is that only businesses based in Seattle are eligible. There are a few other criteria to qualify:

- Must have fewer than 50 employees or earn less than $7 million in annual revenue

- Must have a physical presence within a few blocks of Amazon’s office buildings in Regrade, South Lake Union, or Bellevue

- Must be open to the general public

- Must be reliant on foot traffic for business

We should also mention that there are city-specific programs for most major cities and many smaller towns as all. Check with your city or municipality to see what sort of programs they may have organized to help small businesses combat the effects of the coronavirus crisis.

5. State-Specific Programs

Part of the beauty of living in the United States is that, at the end of the day, each state retains a level of independence. This gives state governments the ability to develop their own unique strategies to tackle the economic impact of coronavirus (something that’s been evident in the resistance many governors have put up against President Trump’s ‘Opening Up American Again’ plan).

Indeed, most states have launched their own financial relief programs to help individuals, families, and businesses make it through this tough time.

Use our interactive map to see what initiatives your state has started to fight against the coronavirus crisis.

Become united

The sands of the economic landscape continue to change as coronavirus news and updates keep pouring in. It can be very difficult to navigate these tricky waters, but it’s not impossible. Staying informed is important, yes. But one of the best ways to stay ahead of the storm is actually to communicate effectively with other business owners.

Join the Become Business Owner Community to start sharing questions, answers, and ideas with people in situations very similar to your own. You’ll gain new and interesting perspectives, and may even get help with perfecting your coronavirus survival strategy.