Making business dreams possible

Take control of your funding using our free technology:

- Get tailored business funding options

- Discover how to improve your funding odds

- Smart business dashboard & key insights

Creating a better world of funding for businesses

-

For businesses

Using technology and advanced algorithms, we optimize existing funding and unlock funding for millions of otherwise overlooked businesses

Get business profile -

For lenders

We open up an entirely new market segment to lenders using advanced algorithms and by cross-checking previously unfundable businesses

Join us

-

Error-free

application -

Optimal lenders & terms

-

Funding criteria transparency

-

Step-by-step

funding plan

At Become, we understand that securing a business loan can be a crucial step in growing your business. We have streamlined the application process to make it as simple and straightforward as... Read more

Unsecured loans offer a way to borrow money without needing to put up collateral, making them an attractive option for those who may not have assets to pledge or prefer not to risk them. These loans... Read more

In the dynamic landscape of modern business, cash flow remains the lifeblood of enterprises, irrespective of their size or industry. Small and medium-sized enterprises (SMEs), in particular, often... Read more

Small businesses are the lifeblood of economies worldwide, driving innovation, creating jobs, and fostering vibrant communities. Yet, one of the biggest challenges they face is securing financing to... Read more

Our

solution

-

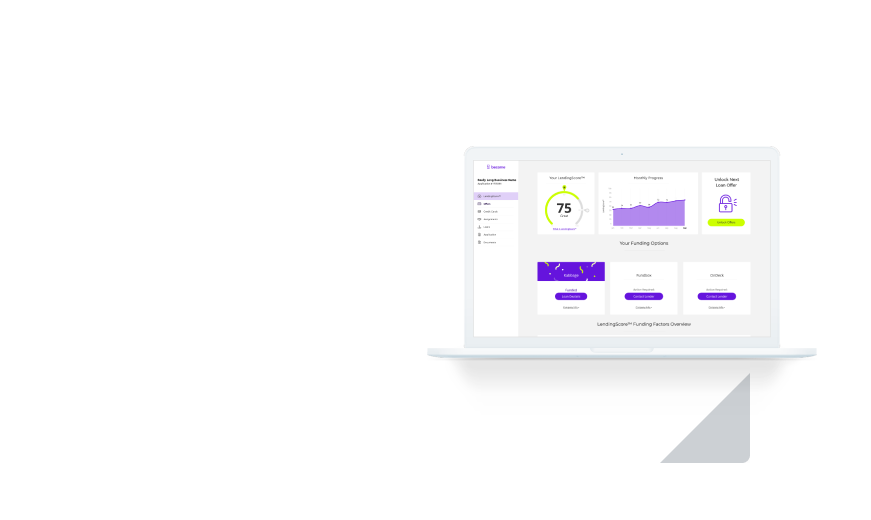

Transparent LendingScore™ Dashboard

Deep business profilingTechnology insights into funding essentials, showing strengths, weaknesses, and step-by-step tasks to improve funding odds and unlock new funding opportunities.

-

Be The One To Choose

Higher approval rateInstead of just applying and praying for approval, you hold the reins and get to claim the best funding solution for your business.

-

Step-by-step Tailored Plan

Continuous funding improvementEach business receives a tailored to-do list with actionable tasks to improve funding odds and continuously unlock better funding solutions.

-

Automated Application Review

Higher approval oddsWith automated application review and cross-validation, errors no longer stand between businesses and their funding.

-

Matching SMBs With Optimal Lenders

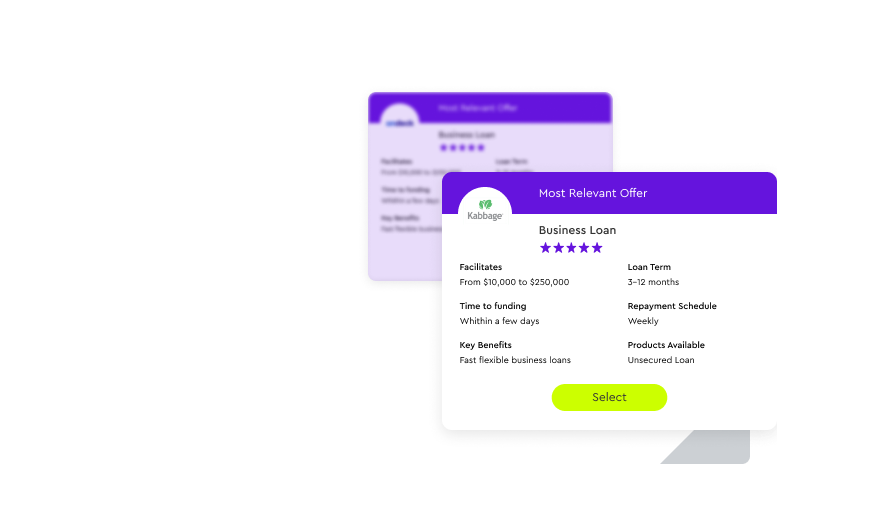

Easy access to tailored fundingBy analyzing 1000’s of attributes, our MatchScore™ algorithm matches each SMB with the optimal funding solutions.

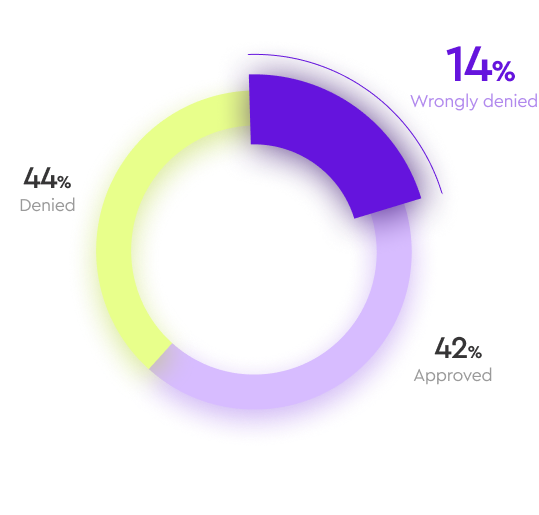

are wrongfully denied funding every year

Businesses who apply for funds using Become's tailored funding solution are around 20% more likely to receive funding *Based on Become's internal information