Can You Get Multiple SBA Loans?

Improving your small business can cost a pretty penny, and business loans can help cover those costs. Small Business Administration (SBA) loans have some of the best terms available for small businesses searching for additional financing. Since SBA loans are so attractive, the question “can you have multiple SBA loans?” is bound to arise. Below, we break down that question to give you an insightful answer. Keep reading…

Can you have multiple SBA loans?

The short answer as to whether or not you can have multiple SBA loans is: yes, it is possible. But, it’s important to address two other questions that will also come into play.

The second question that a business owner may want to ask is, “Should I get multiple SBA loans?” The answer to that question has more details and factors, which ultimately will relate back to the ‘borrowing business’ in question.

If the answer to the second question is ‘yes’, then the next question that naturally arises in a business owner’s mind is, “Can I qualify for multiple SBA loans?” Once again, the answer to that question will depend on specific details relating to the business that is applying for the SBA funding.

In order to flesh-out these answers some more, let’s tackle one question at a time.

Should you get multiple SBA loans?

The question of whether or not you should get multiple SBA loans is one that needs to be approached with careful consideration. The reason is that the risks involved with taking out multiple loans at a time (known as loan stacking) may not be worth the potential benefits. Will several SBA loans help your business do better? That’s really a matter of how you use the loans, and how responsible you are with your money in a general sense.

On a very fundamental level, every business owner needs to be cautious not to stretch themselves too thin by borrowing more money than they can realistically pay back on time. If your business is doing well, and you can afford to take several SBA loans in close succession, then the risk involved is of course lower.

Bottom line: Use your best judgment regarding what you can afford to borrow, and make sure that you abide by all of the SBA’s regulations and rules along the way.

Can you qualify for multiple SBA loans?

Can you have multiple SBA loans? Yes.

Should you get multiple SBA loans? Perhaps, depending on your business’s financial health.

Can you qualify for multiple SBA loans? Let’s find out!

Important: You will not be permitted to exceed the SBA loan program limits. Be sure to review the borrowing limit and qualifications for each of the specific SBA loans programs before applying a second time (more on that below).

Consider the following questions:

1. Is your cash flow strong? Lenders will want to make sure that you’re able to repay the loan(s) that they approve, otherwise they’re putting themselves at risk of not getting paid back! Just like you don’t like dealing with non-paying customers, neither do lenders. Having a consistently positive cash flow is important to get approved for your first SBA loan, let alone a second or third. A healthy cash flow is also crucial to making sure that your business doesn’t stretch itself out too thin.

2. How does your credit score look? Qualifications for SBA funding varies between the different types of SBA loans. Broadly speaking, the minimum credit requirements to qualify for an SBA loan are a personal credit score of 650 and a business credit score of at least 140 (FICO).

If you’re aiming to get approved for another SBA loan after obtaining your first one, there’s a good chance that the lender may require a credit score higher than 650. To improve their odds of SBA loan approval, business owners can improve credit score by using credit cards.

3. Do you have valuable assets to secure another SBA loan? The perspective of most lenders is the more debt you have, the riskier you appear as a borrower. To balance that risk, many lenders will require you to put up collateral. That way, if for some reason you can’t or don’t repay the loan, the lender will be able to seize your valuable assets. If you don’t have valuable assets to use as security for a loan, consider applying for unsecured business loans.

In short: Is it hard to get an SBA loan? For businesses that have a poor cash flow, low credit score, and lack valuable assets to use as security, qualifying for multiple SBA loans will be more difficult.

Why would you need multiple SBA loans?

There are numerous reasons why a business owner may need to take out multiple SBA loans. For example, if the first SBA loan you obtained was used to turn a very bare-bones business into a fully-operating enterprise, a second SBA loan might be desirable for:

- Hiring more employees

- Purchasing a new business location

- Buying or leasing equipment

- Improving your marketing strategy (to include social media marketing, for example)

- Scaling up business

If you were to use a second SBA loan for one of the purposes above, you might then take a third SBA loan to check another line off that list. The task of improving your small business entails a lot of different steps that each have a price attached. Whatever the purpose is, you can use multiple SBA loans to cover the costs involved in improving your business.

Borrowing Limits for SBA Programs

What is the maximum SBA loan amount? There are different borrowing limits for the different SBA loan programs, but the maximum SBA loan amount (whether you’re combining SBA loans or not) is $5 million.

Of course, the type of business will affect the kind of industry loans a business needs, as well as the specific circumstances that business finds itself in. Be sure to weigh your options carefully in order to choose the right funding solution for your business.

Borrowing limits for different types of SBA loans:

|

SBA Loan Type |

Borrowing Limit |

|

Standard 7(a) Loan |

$5 million |

|

7(a) Small Loan |

$350 thousand |

|

504 Loan |

$5 million |

|

Express Loan |

$350 thousand |

|

Export Express Loan |

$500 thousand |

|

Community Advantage Loan |

$250 thousand |

|

Microloan |

$50 thousand |

|

Disaster Loan |

$2 million |

Combining different types of SBA loans

Other than the borrowing limit, there are no restrictions when it comes to combining different types of SBA loans. Even though different SBA loan types are meant to meet particular needs for business owners, any combination of SBA loans is permitted, granted that the overall amount of financing doesn’t exceed the $5 million cap.

SBA 7(a) loans are designed to be more flexible in terms of what they can be used for, while SBA 504 loans are designed more specifically to cover the cost of equipment, land, or a large construction or renovation project. Be sure to look into the differences between the varying types of SBA loans.

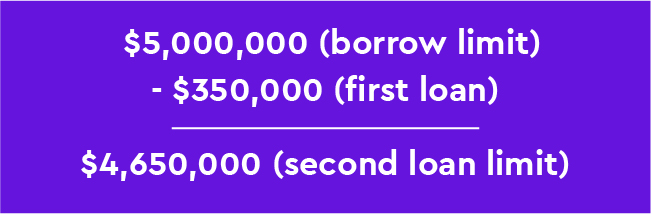

Here’s an example to illustrate this point more clearly:

Let’s imagine that your first SBA loan was an SBA Express Loan of $350,000 that you used to improve your business’s marketing, and you wanted to then apply for an SBA 504 loan to buy new equipment that will allow you to scale up the business. That second loan amount could not be more than $4.65 million.

Can you have multiple SBA loans? Yes, with restrictions. Now that you know you can take out several SBA loans, you should also know what potential dangers come along the way.

The dangers of stacking SBA loans

When a business owner takes out several loans at a single time, it’s called loan stacking. Loan stacking in and of itself is not necessarily a dangerous practice. There are other factors to consider when deciding whether or not to take several loans out together.

Why do people stack loans?

To put it plainly, it takes money to make improvements to your small business. And, oftentimes, small business owners will want to take several steps at a time, which will ultimately mean more costs to cover at once. So they’ll take out a few business loans together in order to meet those varying expenses.

Why is loan stacking dangerous?

The problem with loan stacking doesn’t have so much to do with the fact that several loans are being taken at once. The issue has got more to do with the reason for taking out several loans at a time, as well as the financial health of the business in question.

So, is the business owner taking out several loans in order to use one loan to cover the costs of another? Or, is the business owner taking out multiple loans just because it’s available? If the answer to either of those question is yes, then that business owner is creating a dangerous financial situation for the business that they’re looking to improve. This is what is meant by ‘stretching out too thin’.

The types of loans that a business will be able to stack will often be very expensive loans to take. Plus, the more loans a business takes, the more revenue goes to paying those lenders back. That leaves very little money for the business to use for important, even fundamental operations.

Bottom line: Loan stacking can be dangerous if you’re already in a tight financial situation, as it may dig you increasingly deeper into a hole of debt. Unless you’re absolutely sure you can afford to pay back several lenders at once and keep the business running at full capacity, it’s probably a better idea to avoid loan stacking.

How to apply for SBA loans

Become is revolutionizing the business lending process with the use of advanced algorithms. The proprietary technologies at Become are making the process of applying for SBA loans easier and faster than ever. Plus, the approval odds are improved for small businesses seeking to obtain SBA loans through Become.

Step-by-step guide for applying for SBA financing:

- Choose your desired loan amount and select ‘Get Loan Offer’

- Fill in the requested information (including time in the industry, revenue, business, etc.)

- Submit your business’s checking account information for analysis

- Wait for offers. You can also review your status by clicking ‘Access Your Loan Application’

- Review offers and select your preferred lender

- Receive the funds to your business checking account

- Review your tailored LendingScore™ dashboard to improve your funding options

- Improve your rates – if your LendingScore™ is insufficient, follow the personalized plan (8-12 weeks to unlock funding)

Boost your small business

When applying for small business financing through Become, the answer to the question “Is it hard to get an SBA loan?” is a resounding “No!” SBA loans are among the best types of business financing available, so what are you waiting for? Get started on improving your small or medium-sized business today with SBA funding.

We hope you find this information helpful in deciding whether or not to take out multiple SBA loans.