Business Loans Requirements Guide: How to Become Eligible for Business Loans

Why do lenders have business loan requirements?

Loan providers take on a risk when they lend money, there’s no two ways about it. Naturally, they’ll want to assess and reduce the amount of risk they take on. In order to do that, lending institutions set parameters (known as ‘business loan requirements’) that outline what it takes for an applicant to receive business loan approval. Before qualifying for a business loan, applicants will first have a broad array of their financial factors assessed, which indicate how likely and how able they are to repay the amount loaned.

Why do requirements exist when applying for business loans? Let’s use an example to illustrate the answer to that question:

A little more than a decade ago, in 2008, the Great Recession shook the American economy to its core and brought into question many of the practices that were taking place in certain industries – namely real estate mortgages. It’s a long story, but in short, financial institutions were giving homeowners access to capital in the form of subprime mortgages when it was apparent that those homeowners would either not be able to pay back the loan or have an extremely difficult time doing so. In other words, banks were giving money to people who they knew wouldn’t be able to pay back. The result was the worst financial meltdown since the Great Depression back in the 1930s.

Why can’t lenders just check my business loan eligibility based on my credit score?

Credit scores will certainly play a role in the ability for owners to qualify for small business loans. While credit scores do act as a window into a borrower’s creditworthiness, that ‘window’ offers just a small peek into the overall ability for a business to repay a loan.

Creditworthiness – the extent to which a person or company is considered suitable to receive financial credit

Lenders are well-aware of that fact, which is why their analysis of a business’s financial factors includes other factors such as monthly revenue, monthly bank balance, existing loans, and many other business loan criteria.

Keep reading for the full list of business loan criteria…

Business loan eligibility: What’re the odds?

The fact is, more than 80% of small businesses are denied funding through their banks. But when you’re applying for a business loan, what do banks look at? While we assume that many of the factors that Become assesses with its technology are also taken into consideration by traditional lending institutions, the fact is we can’t be entirely sure. And neither can you. That leaves a lot of room for uncertainty on behalf of the business loan applicants.

What’s more concerning is that almost 60% of small business owners that applied through online lenders were denied a loan, and more importantly have no idea why they were rejected.

Imagine trying to get a loan from a bank and getting denied. Then applying for a loan through ‘more promising’ avenues online, and still reaching a dead-end. We understand how frustrating a process it is for small businesses to obtain financing, that’s why Become is dedicated to improving their funding odds.

How?

Become’s services provide insights into how lenders see you – something you won’t get anywhere else! That’s just one of the many ways that Become stands apart from all other alternative online lenders as a fundability optimization platform. Find out what our lending partners take into consideration when assessing business loan approval.

What business loan eligibility criteria will you need to meet?

Below is the complete list of business loan requirements that lenders in the Become network will take into consideration. Just keep in mind that while each factor contributes to a loan provider’s understanding of how reliable the borrower is, no single factor can be used to make an honest and accurate determination of business loan eligibility.

Business loan eligibility criteria:

1. Credit Score*

In most business loan applications, there will be a section that requests information about the applicant’s credit score. This score acts as an insight into the applicant’s creditworthiness (defined above). The range of possible credit scores ultimately depends on which credit bureau you’re getting scored by, but for the 90% of lenders who use the FICO credit scoring service, the range is from 350 to 850.

Ultimately, businesses with stronger credit scores will have access to more and better loan options than those with weaker credit scores. That said, with dozens of top lenders in Become’s network, many are still able to help small businesses with poor credit scores get funded (those with super low credit scores can still qualify for credit cards, for example).

2 / 3. Non-Sufficient Funds*

Known in Australia as Dishonours**, non-sufficient funds (NSF) is the status that is attributed to an account when it doesn’t have enough funds available to cover the [attempted] transactions. Typically, there is a fee that is charged by the bank when a non-sufficient funds alert is made on an account. Occasionally, a merchant may also charge their client a penalty if an attempted payment is denied because of non-sufficient funds.

While there isn’t any maximum number that a lender will look out for, the rule of thumb is that the more NSF alerts there are on an account the worse. If a business’s account is repeatedly showing NSF alerts, that is an indicator that the business has difficulties making payments on time. Of course, that will make lenders strongly reconsider the creditworthiness of a given applicant.

4. Monthly Deposits

This factor may seem fairly self-explanatory, but there are important details to be mentioned. The number of deposits that a business makes into its bank account, the amount of each deposit, and the consistency of deposits from one month to the next are used as measurements for how healthy a business is performing.

With dozens of lending partners that applicants may qualify with by applying through Become, there isn’t a universal minimum number of monthly deposits that lenders will require. Plus, what each lender counts as a deposit will differ (some count ATM deposits and account transfers, while others don’t).

The bottom line is, more and bigger monthly deposits (however they’re defined) are advantageous in qualifying for a business loan. But, they’re still only one part of the larger list of business loan requirements.

5. Business Age

New business loan requirements (or startup business loan requirements) are a little bit less clear simply because the definition of a ‘new business’ or ‘startup’ is not universally agreed-upon. Some sources will say a new business is one that hasn’t yet officially started, while other sources will say that a startup business can include businesses that have been operating for 3, 6, or even 12 months.

While there are several lending partners in the Become network that can provide financing to businesses as young as 3 months of age, most of our partners include in their business loan criteria that a business be operating for at least 6 months. New business loan requirements differ from older small business loan qualifications in the general sense that the more experienced a business is, the easier it will be to qualify for business financing. Fortunately, there are useful steps that can be taken in order to obtain startup funding.

6. Monthly Revenue

As opposed to ‘monthly deposits’, which is a count of how many deposits your business makes into its bank account per month, ‘monthly revenue’ is the amount of money that your business brings in every month. What lenders will consider when determining business loan approval is not so much the amount of money that your business made this month or last month or next month, but the consistency of the monthly revenue from one month to the next.

For example, if you typically make $10,000 in monthly revenue, but this past month your business had to recover from a disaster and your revenue was only $2,000, it wouldn’t make much sense to assess your creditworthiness on that slower month. On the other hand, if your average monthly revenue was around $2,000 but this past month the sales were spectacular and you had $10,000 in revenue, it also wouldn’t make sense for a lender to assess your creditworthiness on the one month that stands out. Generally speaking, the larger and more consistent your monthly revenue is, the better the chances you’ll have at qualifying for a business loan.

7. Existing Business Loans

When it comes to small business loan qualifications, this is one of the most straightforward. Loan providers will be very hesitant to lend money to a business that already has outstanding debt, particularly if it’s in the form of existing business loans. If you’re demonstrating difficulties with repaying the small business loans that you already have, it will be apparent to a lender that you’ll likely have a hard time paying them back as well.

If your business has existing business loans and you’re aiming to get business loan approval, you’ll want to first concentrate on consolidating your existing debt and paying it off. The odds are slim that you’ll find yourself qualifying for a business loan if you have other loans that you already have a hard time repaying. That being said, if you handle your existing loans responsibly, it is possible to take out multiple loans (including mutliple SBA loans).

8. Negative Balance Days

On the odd occasion, even the best of us can miscalculate and overdraw or overcharge our bank account. It’s not the end of the world, because most bank accounts will include alert services that will give you a heads-up before a negative balance turns into a bigger problem.

Typically your bank will give you a chance to make a quick deposit before any penalties result from a negative balance. But, if too much time passes and you don’t realize or don’t do anything about a negative balance, it will not only be on your financial record but it will also negatively impact your credit score. Lenders will be able to see how many negative balance days you have on your account and, of course, the more you have the worse it reflects on your creditworthiness.

9. Bank Balance

Similarly to the way that lenders will assess your monthly revenue, the consistency of your bank balance will have an impact your business loan eligibility. If one month you have $10,000 in your business bank account and the next month there’s only $2,000, it will likely raise some eyebrows. Qualifying for a business loan will depend on your ability to demonstrate your reliability as a borrower. That means making payments on time and in full.

If your bank account fluctuates dramatically from month to month, it’s a signal to lenders that your business is unstable and inconsistent – not the type of characteristics a loan provider wants in a borrower. If the root of a shaky bank balance is having so many unpaid invoices, you’ll want to work on finding strategies for dealing with non-paying customers.

*Only for those in the U.S.

**Only for those in Australia

How can businesses ensure they meet the requirements?

With so many different funding factors to take into consideration, it’s not always the easiest thing to keep them all up to par. Plus, if you’re having trouble qualifying for a business loan to begin with, the odds are that you won’t know why you’re being rejected from other lending institutions. So how are you supposed to improve your business loan eligibility if you don’t know what’s affecting it? That’s where Become offers unique services that set it apart from other business financing institutions.

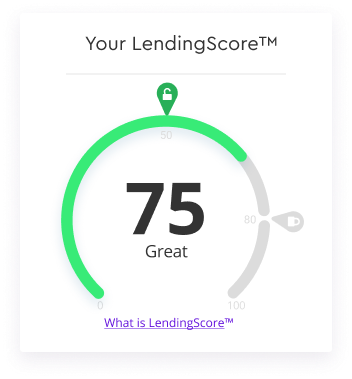

What is LendingScore™?

Become uses its proprietary LendingScore™ technology to quickly and accurately assess a business’s entire financial profile (made up of the 9 funding factors listed). With advanced algorithms, the LendingScore™ platform is able to analyze each of the funding factors and then present them in the form of a score out of 100.

A business’s LendingScore™ represents how loan providers view that company’s business loan eligibility. Scores below 50 are deemed incapable of qualifying for a business loan and still need to improve their business loan criteria.

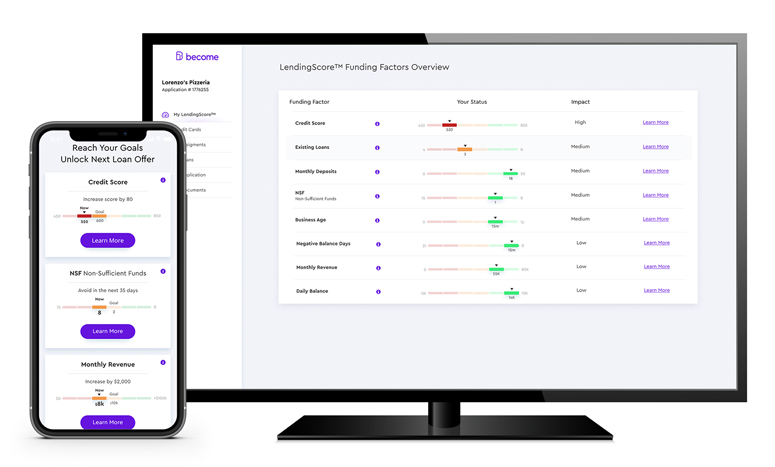

In-depth assessment of a business’s financial profile is only the first step in the LendingScore™ experience. All of the results of that assessment are then illustrated through the intuitive and interactive LendingScore™ Dashboard which provides up-to-date information regarding the status of each funding factor.

How does the LendingScore™ Dashboard help businesses improve their fundability? We’re glad you asked! Each business’s LendingScore™ Dashboard is tailored to its particular business financial profile, which means that Become customers aren’t just receiving generic advice on ‘how to improve their finances’ that they can find anywhere.

Become provides guidance on how you can optimize your fundability by taking specific steps to improve specific factors that are standing in the way of you qualifying for a business loan.

The LendingScore™ Dashboard uses visual aids to show where your business stands on each funding factor, along with a goal of what you need to achieve to become more fundable. The tailored dashboard will show you a goal of how much you need to improve each specific factor in order to unlock a new funding opportunity. You can then deep-dive into each factor to learn more on how to improve it – this is where you’ll find tools, tips, and advice.

Each factor will have an ‘impact level’ (high, medium, or low) so that you can prioritize which funding factors you need to work on first. By improving those higher impact factors, you’ll have a stronger positive effect on your LendingScore™. Additionally, Become will show you a priority list of which factors hold more weight so that you know which ones to focus more to increase your chances of obtaining funding.

What are common loan application mistakes?

This is one of the questions that most, if not all, business owners find themselves asking when they start their journey towards business loan approval. The most common pitfalls that business owners face when they start a new company are:

- Failure to prepare

- Insufficient funding

- Picking a bad location

- Lack of online/social media presence

- Poor management

For many years, the second item on the list above (insufficient funding) has been an immensely widespread problem for small and medium sized businesses.

As a result, Become created a solution that would improve the approval odds for businesses seeking financing. Become has been operating for nearly 3 years now and has helped provide over $150 million in funding (cumulatively) to thousands of small business owners.

With that in mind, you’re encouraged not to let those pitfalls discourage you! The fact is, no matter how much reading and studying someone does, nothing is quite as good of a teacher as personal experience. By all means, do everything you can to prepare yourself before giving it a go. But at the end of the day, nobody is ever fully prepared for their first attempt at starting a business; you’ll just have to take the leap of faith, spread your wings, and do your best to maintain flight!

If you find yourself having taken a wrong turn somewhere along the way, that’s okay! We’re human, after all. What’s more important is that you learn from your mistakes and improve over time.

Step-by-Step guide for applying for a business loan

Step-by-step guide for applying for a business loan:

- Choose your desired loan amount and select ‘Get Loan Offer’

- Fill in the requested information (including time in the industry, revenue, business, etc.)

- Submit your business’s checking account information for analysis

- Wait for offers. You can also review your status by clicking ‘Access Your Loan Application’

- Review offers and select your preferred lender and terms

- Receive the funds to your business checking account

- Review your tailored LendingScore™ dashboard to improve your funding options

- Improve your rates – if your LendingScore™ is insufficient, follow the personalized plan (8-12 weeks to unlock funding)