How to Get Funding for Your Small Business in 2021

Developing a business from the ground-up is not a task for the thin-skinned or weak-hearted. Starting a company can be the first step towards financial freedom, but achieving lift-off comes with challenges and risks. One of the most fundamental hurdles that need to be cleared from the get-go is figuring out how to get funding.

New business owners will face a number of difficulties when it comes to securing funds in 2021.

Difficulties in securing funds include:

- Creating a scalable business model

- Making plans for the future, and aligning goals with the budget (and vice versa)

- Determining the right loan amount

- Finding investors that fit well with the business’s mission statement

- Building a network with strong connections

Below, we provide information and insights regarding small business lending trends so we can show you how to get funding for your business. Keep reading to discover more…

The small business economy in 2021

According to the United States Small Business Association (SBA), more than 627,000 new businesses set up shop every year. At the same time, roughly 595,000 business shut down annually. That’s staggering, but what is more concerning is the whopping 20% of new companies that aren’t able to make it through their first year in business. And while that might not sound so bad, the other 80% shouldn’t let their guard down so quickly; 50% of new businesses don’t make it past their fifth year in business.

Another interesting point worth highlighting is the fact that these statistics are rather consistent from one year to the next. In other words, the survival rate of new businesses is not dramatically affected by larger economic fluctuations.

This is important to note since many prospective business owners will want to wait for ‘the right time’ to make the leap of faith. The lesson is, if you’re thinking about starting a business, you should be more concerned with having a strong business plan than you are concerned with the state of the economy. A successful business will weather the storms that eventually come, so focus on building a strong business foundation that can resist the sands of time.

If you’re not sure how to go about it, you can start getting prepared with the section below. Scroll down to learn more about why some small businesses fail.

Why do some small businesses fail?

While it’s useful to know how many businesses survive and how many fail, what’s more useful is knowing why some businesses do better than others. Below, we’ll describe six of the top reasons why some small businesses crash and burn.

Top six reasons why businesses fail:

1. Lack of preparation

We have a saying here at Become: “Preparation plus opportunity equals success.” There’s plenty to prepare for when you’re drawing up plans to start a business. Many small businesses flatline because they simply failed to plan ahead for the demands of running a company. And, on the contrary, every successful venture started off with a reliable strategy for how to remain in the game.

Key points that businesses should prepare include:

- Assessment of competition

- A clear mission statement, with specific goals and plans on how to reach them

- Industry research

- Marketing and advertising

- Workforce demands

- Balancing finances

- Managing growth

- Potential obstacles and how to overcome them

2. Lack of funding

One of the most common reasons that small businesses fail is a misunderstanding of how much money they’ll need to keep operating after the doors open. Many new businesses miscalculate their funding needs, not knowing that they’ll likely need to cover the costs of their business out-of-pocket for a couple of years before the company’s revenue grows enough to cover the operating costs.

Now, you’re likely wondering how to get funding for your business. That’s where Become comes in. Not only does Become have dozens of lending partners that your business may qualify with, but if you don’t qualify you’ll learn why and gain valuable advice on how to improve your funding odds – for free! You can apply today obligation free to see if you qualify for a business loan from our lending partners.

3. Poor choice of location

As cliche as it’s become, the saying remains true: location, location, location!

Your startup’s success depends largely on whether it’s based in the right area or not. Even the most tried-and-tested business plan would fail if it were located in the wrong place. Think about what services or products you’ll be providing, and whether the demand exists in the area you’re looking to open shop.

Questions to consider when choosing where to open your business:

- Where are your competitors located?

- Where are your customers located?

- How successful have other businesses been in that location?

- How is the traffic? Parking? Accessibility?

- Is the area safe? Clean?

4. Poor online/social media presence

In our world of smartphones and instant access to virtually everything, if your business isn’t online then – for all intents and purposes – it basically doesn’t exist. Okay, maybe that was an overstatement, but the principle remains true. If a potential customer were to hear the name of your business, how would he or she be able to find out more?

Chances are, they don’t want to make a phone call and speak with a representative just to get a clearer idea of what your business is all about. Even the most basic website design would provide clients with the standard info they’d be looking for: what you do, how long you’ve been around, where you’re located, how to contact you, and so on. If your business doesn’t at least have a website, you’re doing yourself a tremendous disservice by severely limiting people’s ability to connect with your company.

Top tip: Tools to build a website include Wix and WordPress – no excuses now! There are also plenty of free business tools that you can use to improve online presence.

If you’ve established yourself a website, the next step is to get on social media. Facebook is the most fundamental of all social media platforms and is nearly as important as having a website. After you’ve set up a Facebook page for your business, you can easily expand to other platforms such as Instagram, Twitter, and even Linkedin.

5. Issues with management

Management issues are something that most new businesses are confronted with, but many are unprepared to handle them effectively. New business owners are often inexperienced in areas of management that have a critical impact on success and survival, including finance, buying and selling, selecting employees, and so on.

Even if you’ve received formal business education, the practice of managing is a challenge for someone without real-world experience. If you haven’t started sharpening your management skills, start learning today, or be prepared to outsource for the expertise you lack.

Management doesn’t end there. Getting the business running is just the start – as a manager, you must stay up-to-date on industry trends, current events, the state of the market, customer data, etc. This will help you stay focused in the right direction, organized in your business plan, and in control of your company’s performance. If you’ve been fortunate enough to get your business established, the last thing you want to do is put it on the backburner.

Lastly, what usually comes to mind when people hear the title ‘manager’ is the person in the workplace that leads the team. The manager should be good at fostering a positive work environment by keeping the energy up, hiring employees that fit well with the team, moderating internal disputes, and continuously thinking of ways to better the business strategy in new and productive ways.

All of these skills come with time and experience, so don’t put too much pressure on yourself if you’re still new to business management.

6. Wrong reasons for starting the business

When you were growing up, chances are high that you were taught some sort of ‘golden nugget’ of work advice along the lines of “If you love what you do, you’ll never work a day in your life”.

It’s great to enjoy what you do for a living, but the reality is enjoyment doesn’t pay the bills. But the opposite is true as well – getting the bills paid doesn’t equate to happiness in life. Many new business owners see their companies fail because they didn’t start for the right reasons, and failed to do their due diligence before opening shop. You shouldn’t go into business because you want to make a lot of money, or because you’re sick of working for other people. Those are good motivators for action, but not sustainable as reasons for running a business.

Good reasons for you to start a business include:

- You get back up after being knocked down. A successful business owner isn’t one who just avoids difficulties, but one who can bounce back stronger and learn from the past

- You show determination in your pursuits and patience throughout the journey

- You are able to deal positively with people of different walks of life

- You strongly believe in what you’re doing and have found a need for your service/product

- You do well at operating independently, particularly under pressure

Is there inequality in the lending industry?

The unfortunate reality is that prejudices do exist in our world, and the lending industry is no exception. Prospective business owners, regardless of race or gender, struggle with trying to figure out how to get funding for startup businesses. On top of that normal level of difficulty, the added obstacles that some people face on the basis of their identity is truly a shame, to say the absolute least.

Inequality in the lending industry is measurable. Findings from a 2017 government report on small businesses show that more than 50% of black-owned firms who applied for a loan from the bank were turned down, despite the fact that black-owned firms were the most likely to apply for a loan from the bank. Moreover, black-owned businesses were the most likely to fail at obtaining full-funding from a bank, and they were more than 10% more likely to fail than the next-highest group.

Women are also victims of prejudice, according to the same report – “female-owned firms were slightly less likely to apply than their male counterparts but more likely to be turned down.” And the opposite was true as well. The authors found that, despite the fact that male-owned businesses were less likely to apply for a loan than female-owned businesses, the approval rates were similar.

These findings are absolutely something to be concerned about, so what can be done to lessen the effects of prejudice on your chances of getting approved for a business loan? That’s one place where Become can proudly offer up a real solution. Simply put, the digital lending services provided by Become totally take the loan applicant’s personal identity out of the equation, because it shouldn’t have been in the equation to begin with!

Our technology assesses relevant factors to your business’s fundability, including credit score, monthly revenue, time in business, etc. If before you were wondering how to get funding for a business, you now have a viable course of action.

See the complete list of funding factors below:

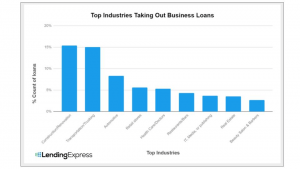

Which industries are most likely to apply for financing?

Small businesses come in all shapes and from a wide variety of industries. We’ve analyzed our data from 2018 and produced the graph below to show you which industries were the most likely to take out a business loan.

From more than 60 industries, we provide you with the top 9:

But what are the reasons that small businesses in some industries seem to know how to get funding more successfully than in others? The answer may lie in the nature of those industries which ranked highest on the graph above.

Construction and renovation landed in first place, receiving roughly 17% of all loans provided. There’s a constant need for this industry, as cities continue expanding and new residential buildings and offices are needed to sustain growth. This means that, in order to keep up with the demand of the industry, those companies need to hire more workers, buy more equipment, and so on. That explains why the construction and renovation industry is number one with regards to the number of loans taken out.

Transportation and trucking came in second place with approximately 15% of the loans provided in 2018. In case you’re not in that industry and weren’t aware, there’s a huge demand for transporting not only people but goods as well. As mentioned just above, cities are constantly growing, and that requires a steady flow of both material and human resources. Since that demand is neverending, transportation and trucking companies frequently need to enlarge their fleets and hire new drivers, which is why they take out so many loans.

Ultimately, it is important to highlight that the likelihood of qualifying for and receiving a loan from Become is not based on the industry which your business is in. The above statistics represent broad and general small business lending trends. Your individual business’s chances of obtaining funding through Become are based on your tailored LendingScore™, which assesses your credit score, the age of your business, monthly revenue, etc. in order to determine your fundability.

One important note: Of course, the type of business will affect the kind of industry loans a business needs, as well as the specific circumstances that business finds itself in. Be sure to weigh your options carefully in order to choose the right funding solution for your business.

How to get small business funding in 2021

We don’t need to tell you how difficult it can be to obtain funding for a startup or small business, but we will. It can be stressful, frustrating, and discouraging. So we’ve produced this section to set your mind at ease and guide you towards improving your chances of getting funded.

The first thing to do is research the different loan options available to see which of them fit your business needs the best. Don’t sweat it, we’ve already done the research for you.

Best loan options for small businesses:

- Startup business loans – this is the solution for how to get funding for startup businesses right here; these are particularly helpful if you have the idea for a business, but haven’t obtained the funds needed to put your plan into action. You don’t need to own a business in order to qualify, which offers a great advantage for prospective owners.

- SBA loans – The U.S. Small Business Administration (SBA) offers assistance to small businesses by guaranteeing up to 85% of a business loan amount. The ‘safety net’ that SBA loans provide to borrowers also serves as an incentive for lenders to approve loan applications. So even if you’re unsure whether or not you’ll be able to pay the loan back in full, SBA loans should be taken as a serious consideration.

- Commercial business loans – These can be used to cover the initial costs of establishing your business. As opposed to applying for multiple loans, one commercial business loan can cover all costs. Interest rates are typically on the lower end of the spectrum, and repayment terms are long (which means smaller payments).

Now that you have a few loan options, it’s time that we explain what you really wanted to know: how to get funding for a business. Luckily for you, we’ve narrowed the process down to just 5 steps to keep it simple and easy.

5 steps to improve loan approval odds:

- Understand which loan option fits best with your business profile and needs

- Review your financial profile, know your credit score/history, and correct any errors

- Reduce your debt-to-income ratio, and boost your net income

- Arrange documents in order to provide a cosigner or collateral, if necessary

- Get rid of your existing debt as much as possible

Working on those steps will improve your loan approval odds and bring you one step closer to obtaining funding for your business. Yet, as short-and-sweet as that list is, we understand that it can still be a bit confusing to put those instructions to action. The plain truth is, if it were easy you wouldn’t be reading this! That’s why we’re here to provide you with the guidance you’ll need to get your business funded. Keep reading to find out how we use technology to improve your funding chances.

Improve your funding odds today with LendingScore™!

LendingScore™ is the name of the technology that we use to provide a financial business profile of your company. We use your company’s financial profile to determine which factors are impacting your loan approval odds.

As your company’s profile is scanned by our advanced algorithms, different point values are assigned to the different financial factors in order to produce a LendingScore™ (a score based on a scale out of 100). As your LendingScore™ increases you unlock new and better funding opportunities.

There’s also the LendingScore™ dashboard which shows you all of the aspects of your business profile along with all of the funding options your business qualifies for. Everything is provided in one place, so you don’t need to log in on multiple websites and you don’t need to click back and forth between different profile pages. Best of all, the LendingScore™ dashboard also provides you with advice on how to fix the factors that are impacting your score.

What are the best business loan alternatives in 2021?

Business credit cards, personal credit cards, and personal loans.

Even with all the help in the world, some prospective business owners just can’t seem to catch a break with obtaining the funding they need to get the ball rolling. If you can’t figure out how to get funding for your business through a business loan of one sort or another, there are alternative options worth exploring.

While you may have some reservations with the idea of using a credit card to start your business, you’d be surprised to learn that even some big-name entrepreneurs have done exactly that. One of the co-founders of Google, Sergey Brin, was quoted in an interview as saying, “When we decided to start a company…we spent about $15,000 on a terabyte of disks. We spread that across three credit cards.”

There are many credit card companies to pick from, each with many types of credit cards that they offer, and each credit card comes has different qualifications, interest rates, rewards, and so on.

Advantages to using a credit card as an alternative to a business loan:

- Ease and convenience of getting financing

- Rewards for using the card

- 0% interest for the first year (for many, if not most cards)

- No collateral

- Use as-needed

If you’ve done all your research and you still feel that using a credit card is not how you want to get funding for your business, one more alternative to a business loan is to take out a personal loan. Of course, the obvious way to use a personal loan would be to make the purchases you would otherwise have made with the funds from a business loan.

The less-obvious way to use a personal loan is as a way to consolidate your existing debt, reduce the interest rate on that debt, and effectively help to improve your credit score. A better credit score means a better LendingScore™, and better odds at getting approved for a business loan.

The long and short of it

We’ve said it before and we’ll say it again: starting a business is not a walk in the park. It takes dedication to the vision, grit in the face of difficulties, and creativity in finding solutions. But nothing worthwhile ever came easy, and achieving the establishment of your business will be just the beginning of the journey. We’ve now given you everything you need to know about small business lending trends for you to figure out how to get funding for a business. Don’t get caught in the same pitfalls that have spelled doom for so many other small businesses. We encourage you to use this information to not only establish your business but to guarantee that it thrives for years to come.

Feel free to bookmark for future reference, share with a friend, and comment below if you have any feedback!