What is Good Debt and Bad Debt?

Debt – the four letter word that we’ve learned to dread and to avoid at all costs. The advice you may have heard growing up was to not spend money that you don’t have. The truth may come as a shock to you: 80% of Americans are currently in debt.

Let that sink in for a minute.

So if debt is so terrible, why have the vast majority of Americans decided that the reward is worth the risk? Why is debt good for a company? Keep reading to find out…

What is good debt?

The term ‘debt’ typically has a bad rap – but there are types of good debt as well.

What is good debt? Simply put, good debt is a form of investment that will either:

- Add value

- Grow in value (as opposed to devalue) over time

- Or will develop into a source of income in the long-run

Using the word ‘good’ or ‘bad’ can be misleading. The contrast isn’t used to describe a specific dollar amount. The amount of debt that your business will be comfortable handling might be way too much for another company to take on, and vice versa.

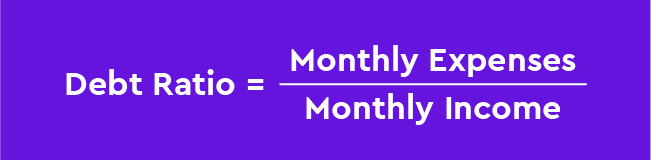

So how are you supposed to determine whether or not you’re taking on too much debt? Short answer: your debt-to-income ratio. To calculate your debt-to-income ratio, add together all of your monthly expenses, and then divide that total by your monthly income.

It’s important to keep in mind that you shouldn’t aim to keep your debt under a certain dollar amount. Instead, the goal should generally be to keep your business’s debt-to-income ratio at 43% or below. If your debt-to-income ratio exceeds 43%, then your chances at getting approved for a qualified mortgage decrease dramatically.

You asked “what is good debt”, and we answered.

Now that you know how to measure and assess the size of your debt, the next question to ask should be “what are the types of good debt?”

Broadly speaking, anything that you spend money on today which will improve your net worth or help you generate income later on down the line will qualify as ‘good debt’.

Types of good debt include:

1. Student loans

Commonly referred to as an investment in your future, student loans are one of the most popular forms of good debt in the United States.

In 2017, the median weekly earnings for people 25-years and older with a bachelor’s degree was $1,189. Compare that to $718 weekly for those with only a high school diploma, and you’ll quickly understand why student loans are considered a form of good debt.

Interest rates for student loans are usually lower than other types of loans, and the fact is that the highest-paying professions all require higher education. The key to handling students loans successfully is planning ahead and assessing whether the target profession is definitely what you want to pursue.

2. Mortgages

Taking out money to live in a house is one of the best forms of debt to have.

While it’s no secret that the housing market was at the center of the 2008 Great Recession, it has since recovered. According to Zillow, today the median price of homes in the United States stands at $275,000 – that’s a 7.5% increase since last year.

This upward trend is projected to continue over the next year, which is good news for the 63% of homeowners who have a mortgage.

A house bought today for $235,000 which increases in value by 3% every year will be worth $485,000 after 30 years (the typical term of a fixed-rate mortgage). The interest rates can be even higher, and the profit over the long term will prove the worth of this form of good debt.

3. Home equity loans

These are loans that are basically using your home’s value as a guarantee to take out either a lump sum of cash or a line of credit.

The interest rates are comparably low, making home equity loans one preferred way of repaying other forms of debt like credit card debt.

Of course, the variety of ways to use home equity loans is limitless, but many people use them to improve the value of their homes by renovating, adding solar panels, installing a swimming pool, etc.

Home equity loans are another form of good debt that depends on you making wise choices with your funds.

4. Business loans

It takes money to make money. Starting a business, or keeping your current business in good shape, definitely qualifies as good debt.

Business loans are useful if, for example…

- You have a great idea that you dream of actualizing

- Your existing company needs a refresher to keep the cash flow running strong

- You want to take your existing business in a new direction

Business loans are often difficult to obtain from traditional lenders like banks. That’s why Become works with businesses that are striving to reach their goals and helps guide them toward improving their funding odds and secure funding through alternative means.

How to use good debt

You know the types of good debt. Perhaps you’re now wondering how to use good debt.

The process is quite simple.

Follow these steps for how to use good debt:

1. Have a clearly defined and justifiable reason

Without a good reason for going into debt, the debt quickly shifts from ‘good’ to ‘bad’. From a business perspective, of course, the reason you make an investment should be to bring value to yourself.

But while you may want to go back to university to study a long-held personal interest, it may not make sense financially.

Good debt does not include spending money you don’t have on big ticket items for the sake of looking flashy.

2. Make a detailed and organized plan

Determine how you intend on handling the debt before you take it on. If you don’t know how you’re going to repay the debt, you’re essentially digging yourself into a hole without any practical way of pulling yourself out later on.

Lenders will need to know that your business plan is viable. If it isn’t strong enough, it won’t matter if you’re asking to borrow $1,000 or $100,000 — your chances of getting approved will be small.

Not only will making a plan increase your funding chances, but it will also effectively help you run your business in a sensible manner.

What is bad debt?

What is bad debt? Basically, anything that depreciates in value after purchasing it would be considered bad debt.

In discussing good debt vs bad debt, it’s important to highlight that the most crucial factor is your own behavior. Whether you choose a form of debt from the ‘good debt’ column or from the ‘bad debt’ column matters less than how responsible you are with handling finances.

There are many types of bad debt – below we list off the top three types of bad debt we recommend avoiding.

1. Payday loans

There’s a reason payday loans fall under the ‘what is bad debt’ section.

Let’s say, for example, you needed $500 to pay for a repair in your home but didn’t have the funds readily available. A payday loan would front you the $500 without any collateral, but with a very high interest rate (often times $10-$15 for every $100 borrowed, or 300-400% annually). The repayment period is also extremely short, typically by your next payday (hence the name).

This is the first pitfall we mention because it is one of the most difficult forms of debt to rid yourself of once you’ve gotten stuck in the vicious debt cycle that it often results in for desperate borrowers.

Chances are, if someone takes a loan for $500, they may face some difficulties paying back the loan with an additional $75 in interest. Payday loans frequently snowball, and before you know it you may be hundreds of dollars in debt as a result of trying to fix your finances with a payday loan.

The big don’t: Don’t get sucked into payday loans by the attractiveness of quick cash with no collateral.

2. Auto loans

Automobile loans are somewhere in the gray area between types of good debt and types of bad debt.

On the one hand, the cold hard truth is that the vast majority of cars depreciate in value quite quickly – even a brand new car loses more than 10% of its value within the first month.

So, if your plan was to buy a car and leave it in your garage for a few years with hopes that the value would increase, you’ll need to reassess your strategy.

On the other hand, if for no other reason, you may need a car in order to travel to and from work. That in-and-of-itself contributes value and provides you with the ability to earn an income (even more so if your business depends on making deliveries and/or attending meetings in person). Beyond that, the relatively low interest rates (under 5% APR in many cases) that most auto loans offer make them that much more enticing.

The wise route of action is to avoid buying a luxury car like a BMW and stick to the Mitsubishi that will get you from point A to point B in one piece. Or, better yet, use public transportation and avoid the costs of an automobile altogether.

The big don’t: Don’t put your ego above your finances.

3. Credit cards

Perhaps the most notorious of all types of bad debt, credit card debt is definitely not something you want on your shoulders.

Among the 67% of Americans who have credit cards, the average amount owed is more than $6,000. This is concerning, but not as concerning as the interest rates offered by some credit card companies that can exceed 40% annually. This results in the average household paying more than $1,000 in interest on their credit cards every year.

The same way that payday loans can snowball out of control, leaving credit card debt unchecked will lead you towards a situation that will be very difficult to escape from.

The big don’t: Don’t use credit cards to spend money that you don’t have. Do use credit cards to cover regularly occurring expenses as a method of building credit.

Debt vs equity

First, what is the difference between debt and equity?

Equity financing

Equity financing is defined as raising money from a third party investor and selling them a piece of your business in exchange for capital. This might be the right option if you’re at the early stages of your business, or if you believe there’s risk involved in getting the ball rolling.

Upside: You can receive funds without necessarily providing any background of profitability, and on top of that the investor only benefits if your business does well. So it’s within the best interest of the investor to ensure that your company succeeds.

Downside: You’re giving up a part of the ownership of your business, and you may be handing over a portion of control to the investor.

Types of equity financing:

- Friends, family, or another small investor

- Angel investors

- Venture capital firms

Debt financing

Debt financing is defined as borrowing money to help invest in your growth. In comparison to equity financing, with debt financing you’ll want to have a clearer idea of your company’s profitability and ability to repay the loan.

Upside: You don’t need to hand over any portion of your company to the investor, and you maintain full ownership.

Downside: There’s always a risk with borrowing money, particularly if you’re not exactly sure about whether or not you can pay back the investment. The loan provider is less concerned with your company’s ability to thrive and more concerned with just getting their money paid back with interest.

Types of debt financing:

- Term loans – a loan for a specific amount, that is paid over a specific period of time (term)

- Credit cards – a card that is issued by a financial institution that allows the cardholder to borrow funds

- Invoice factoring – selling accounts receivable (outstanding invoices) to a third party in exchange for immediate funds

- Merchant cash advance – funds provided upfront in exchange for a portion of the funds the business receives from future credit card transactions

- Line of credit – essentially the same thing as a credit card, but funds can be accessed through other means (writing a check, withdrawing cash, etc.)

Which to choose, when, and why

Equity financing is best for startups in industries such as high-tech, where the return on investment is projected to be astronomical. And that makes sense, being that angel investors and venture capitalists aim to gain a percentage of ownership of a company that will flourish.

One important note: Of course, the type of business will affect the kind of industry loans a business needs, as well as the specific circumstances that business finds itself in. Be sure to weigh your options carefully in order to choose the right funding solution for your business.

Debt financing is better for established companies that have proven their profitability, and for owners who want to retain full rights of possession. If the risk involved in running your business is minimal, then there’s not such a need to share that little bit of risk at the price of giving over a portion of ownership. And on top of that, the interest rates for debt financing are lower than the return on equity investments.

|

When |

Why |

|

|

Equity Financing |

|

|

|

Debt Financing |

|

|

How debt can help you to avoid cash flow issues

Having a healthy cash flow is crucial to developing and maintaining your business’s value. Debt may seem counterintuitive to keeping a positive cash flow, but, if handled wisely, debt actually can be the key to sustaining a strong cash flow.

Getting a line of credit is one of the most practical forms of debt that can be used to manage cash flow issues. But why is debt good for a company?

A business line of credit is a type of good debt because:

- It provides readily available cash upon request

- The interest rates for a line of credit are significantly lower than the rates for other types of business loans

- You’ll only pay interest on the amount you use, not the entire amount of the line of credit

If your business is facing cash flow issues, don’t discount the usefulness of debt. The important thing is not avoiding debt, but learning how to use good debt.

Debt is a tool that can hurt or heal – the effect that it has is a result of the manner in which a uses it.

Establishing a healthy debt level

We’ve covered good debt vs bad debt – now we’ll fill you in on how to use good debt to establish a healthy debt level.

Questions to ask yourself in order to maintain a healthy level of debt:

- Are you incurring this debt in order to obtain something that will appreciate in value?

- Are you able to manage the debt and make regularly scheduled payments on time?

- Is the interest rate affordable? Will it change?

- Is the debt limited? Meaning, is it a revolving account like a payday loan or credit card?

- Are you sure that this debt is completely necessary? Can you avoid this expense?

If you can answer ‘no’ to any of the above questions, you should probably avoid that debt – or at least reassess your plan on how to manage it.

If your answer to those questions is ‘yes’ across the board, then the next step is to make sure you don’t take on too much debt. Even for types of good debt, too much can be harmful to your business.

Good debt vs bad debt – The perfect ratio

A debt ratio is calculated by dividing the total liabilities by the total assets. If you are financing your business with debt, the debt ratio will be higher.

Typically, the target debt ratio is said to be 0.40 (40%) or lower. Debt ratios over that may raise doubts among lenders about the ability for the debt to be repaid. Too much debt will drag on cash flow and can ultimately result in the need to declare bankruptcy.

But it’s not enough to focus on the ratio itself – in order to determine whether it’s a good debt ratio or a bad debt ratio, you’ll also need to consider the form of debt and the financial status of the business.

Balancing your debt ratio:

- High debt ratios – even debt ratios as high as 0.60 (60%) aren’t necessarily disqualifiers for getting approved for a loan. The determination as to whether the debt ratio is ‘good’ or ‘bad’ is made by assessing many factors, including the industry the business is in, payment history, credit worthiness, and so on.

- Small debt ratios – it’s also important not to have a debt ratio that’s too small. It seems a bit paradoxical at first, but investors won’t normally be jumping at the opportunity to invest in a company that has an extremely low debt ratio.

- Zero debt ratios – this means that the company in question doesn’t borrow at all, signifying the reluctance of the business-owner to take risks. It also means that shareholders have less to gain, as the company’s returns will be limited.

Bottom line: there’s also risk involved in extremely low debt ratios. The debt ratio ‘sweet spot’ is somewhere between 0.3 and 0.6 – you’ll have to investigate the investors you intend on approaching, what the debt ratio was over other companies they have funded, and so on.

In a nutshell

We’ve delved deep into the discussion of good debt vs bad debt. When we started, you may have been wondering “why is debt good for a company”. You may have even flat-out believed that debt is a bad thing.

Now you’ve learned that there are such things as types of good debt, and you’ve even learned how to use good debt. Yes, there are types of bad debt that should be avoided. But what ultimately designates a type of debt as ‘good’ or ‘bad’ is how you use it.

The lesson to take away is that learning how to use good debt is crucially important to the health of your business. So start with the info that we have provided you here, and don’t hesitate to bookmark this page for future reference.

If there are any questions you feel were left unanswered, please feel free to comment below!