8 Reasons Why Your Business Loan Application Was Rejected

Whether you’re a business owner at the very beginning of your venture or simply need some extra cash to expand or keep your business afloat, receiving funds can make or break your business.

Hearing ‘rejected’ can be as heartbreaking as trying and failing to pursue your teenage crush but there it is – rejected.

But don’t close your doors just yet, like anything in life, there are logical reasons as to why your business is being turned down for a loan everywhere…

Top 8 reasons why business loans are rejected

The sooner you understand the ‘why’, the sooner you can reach the ‘how’. How you can turn it all around, and get the funds you need to take your business forward and ultimately reach your goals.

The ability to secure business funding and avoid business loan rejection ultimately comes down to a lenders confidence in your ability to repay a loan. It doesn’t come down to your personal credit score alone, there are other and more specific factors that you also need to understand.

Here are 8 common reasons for business loan rejection

1. Your credit score is too low – for both of your credit scores!

Say wha? You may automatically assume we’re talking about your personal credit score and you were rejected on this alone, but – and this is a BIG but – when it comes to getting a business loan, your business credit score will also be taken into account. Sure your personal score is important, especially if you’re the sole owner of your company, but your business credit score will also be taken into account so be sure to check your credit score.

If you’re scratching your head here then you’re not alone. According to The Small Business American Dream Gap Report, 42% of small business owners don’t know that they actually have a separate business credit score and 82% don’t actually know how to interpret it. This simple misunderstanding is seriously harming business owners and the sooner they understand this element, the better (more on understanding this later).

When it comes to your credit scores, you’ll appear risky if:

- You fail to make payments on time

- Have a lot of outstanding debt

- Have a high credit utilization ratio – more on that in the section below

It is possible to get accepted for a loan if your credit scores are low if you’re performing well in other areas (mentioned in points 3-4 below) which could counterbalance your score.

2. Misuse of your debt utilization

There are so many reasons for business loan rejection but one of the main ones could be to do with your credit utilization rate or ‘balance-to-limit-ratio’. This is basically how much you owe compared to the amount of credit available to you.

When it comes to your personal credit score, lenders want to see that you’re using no more than 30% of the total amount of credit available to you. So for example, if your credit limit for all of your cards is $10,000, you’ll need to keep your total credit card balances below $3,000 in order to keep your credit utilization rate low.

On the other side of things, having no debt at all is another red flag to lenders. A lack of history of responsibly using credit will only highlight your inexperience with debt management – not a good look when it comes to applying for a loan.

Top tip to manage debt utilization:

Keep track of your credit limits for all lines of credit, personal and business credit cards and any other credit sources and make the small calculation to figure out the range you need to stay within. Using the debt service coverage ratio (DSCR) will also help you determine if you can afford to take a business loan to begin with.

3. You’re a very young business

Commercial loan denial reasons can vary greatly and one of the reasons could have something to do with your business’s age.

You probably wouldn’t want to be the first patient of a new dentist trying his hand at pulling out his very first tooth. Likewise, you wouldn’t want to be the first lender handing your money out to an inexperienced business owner whose only been running for a couple of months. Either way, it could all end rather messily (sorry for the graphic analogy but hopefully you get the point).

Lenders feel much cozier wrapped up warm in safety blanket, i.e. when they know they’re lending to an established business, at least 1-2 years old. So, if you have a good monthly revenue, and credit scores but are still being snuffed by the banks and even alternative lenders, it could be coming down to your short time in business.

Other than time travelling to the future, there are viable options for younger businesses in the form of start up loans or crowdfunding. Where there’s a will, there’s a way.

4. You applied with the wrong lender

Every financial institution has different criteria when it comes to providing funding solutions. And while it’s most difficult (and time-consuming) to get a traditional bank loan vs alternative business funding, it may be that there is a lender out there who you could match with, waiting for you to find them.

Need a loan, been refused everywhere? We have a solution:

The solution is right here at Become. We realized this was a big problem for business owners and designed our revolutionary technology to match business owners such as yourself, with lenders they can qualify with.

How to apply:

- Enter your details into the application – apply here for business loans.

- We will cross-reference your data with all of our lending partners to see with which one you can qualify – with no hard credit check in sight.

- You will only be shown relevant loan offers – compare and choose.

If you’re in the ‘I need a loan but keep getting declined’ group then Become can help you find out where you went wrong and what you can do about it…

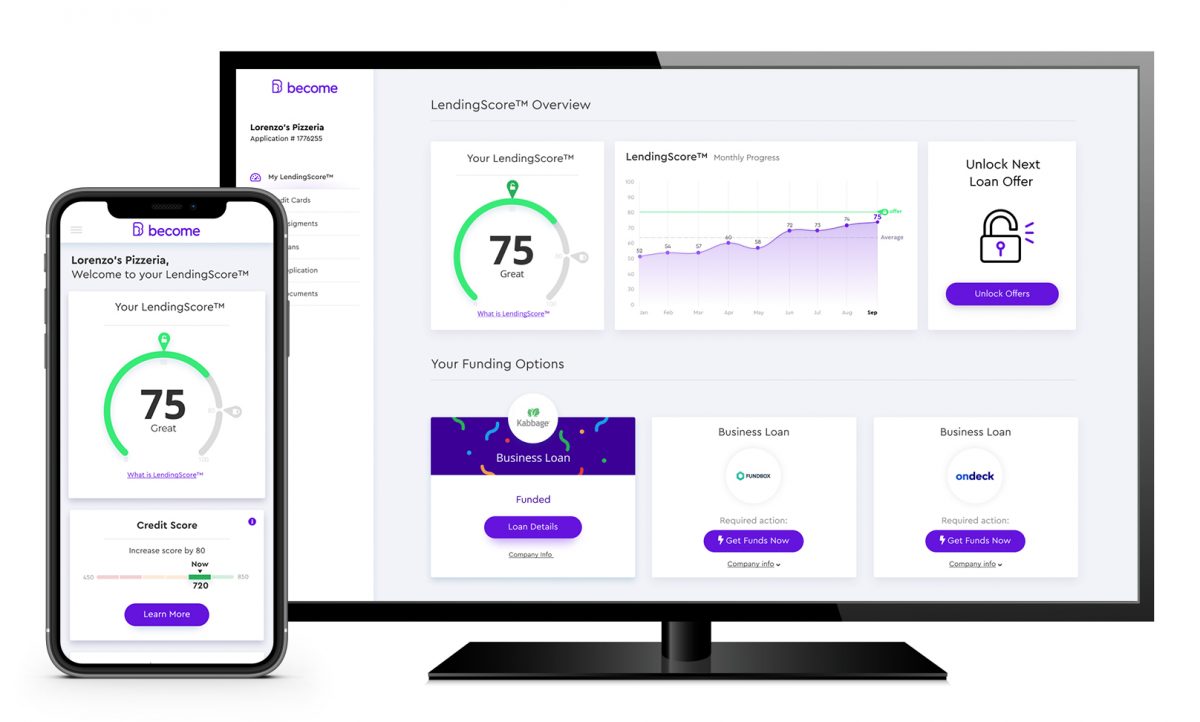

Our LendingScore™ provides you with a personalized free dashboard explaining why YOU were denied a loan with effective ways to increase your chances of getting approved.

5. You applied with too many lenders

There are a couple of main problems with sending off lots of loan applications.

First of all, when you apply with different lenders one-by-one, your credit score will take a hit each time. That means a lower credit score, and even more difficult approval odds for you next time around.

Second of all, if a lender is part of an online business lending marketplace like Become, then they’ll see if you applied through multiple avenues (directly through them, through a broker, through a marketplace, etc.). If you have multiple loan applications going out to the same lender (whether intentionally or not), the lender will often deny you right off the bat. A ‘desperate’ borrower is typically not a sign of a ‘good’ borrower – at least in the eyes of lenders.

6. Your business revenue isn’t quite there

This one is simple, if you aren’t making enough revenue, it shows you may not be capable of paying back your loan. On top of that, if you’re spending more money than what’s coming in, then you will need to work on solving that cash flow problem.

How to work on your cash flow:

- Use effective invoicing systems

- Always have a safety net of emergency funds (and a business disaster recovery plan to use those funds effectively)

- Cut unnecessary expenses

- Learn the difference between gross and net profit

7. You don’t have enough collateral

If you’re aiming to get approved for unsecured business loans, then this won’t be a concern for you. But for many, if not most, other types of financing solutions, lenders will require that you have valuable assets that can be used as security to back the loan.

Collateral can come in the shape of a house, heavy equipment, an automobile, etc. It may appear like a sort of ‘chicken-and-the-egg’ situation where you can’t afford to purchase business equipment without a loan, but you can’t get approved for the loan because you don’t have enough valuable assets.

This is a big reason why you should consider the different types of business loans available at your disposal – and their requirements – before applying.

8. You submitted invalid documents

This may be the most important reason why your business loan application was rejected. Keep in mind that, no matter how impressive your credit score is, how long you’ve been in business, or how strong your revenue is, etc. – if you submit documents that are inaccurate or incomplete, lenders won’t be able to confirm that all of those shining credentials of yours are as great as you claim.

Take the time to go over each step of your loan application with careful consideration so that you don’t waste your time and do damage to your credit score.

As you can see, there are many reasons for business loan rejection, and here we’ve only touched upon a few. At least now, with Become, you can discover specifically why your business was denied a loan and what you can do about it.

What are your next steps after a business loan rejection?

The ways that you can improve your business loan application are a dime a dozen. We’ve narrowed it down to a list of 4 easy-to-follow strategies for boosting your ability to get business funding.

How to improve a business loan application:

1. Utilize LendingScore™ technology

Looking for the best way to improve your business loan application? Look no further! The proprietary LendingScore™ technology developed by Become provides valuable in-depth insights that business owners simply won’t find elsewhere. Not only does the LendingScore™ Dashboard list the precise factors that are impacting your ability to obtain funding, but it also ranks them according to how much of an impact each one has on your fundability. Become then goes the extra mile by giving business owners tailored advice on exactly what you need to change so that your business loan application will result in approval.

2. Build your credit score

A poor credit score will make it more difficult to qualify for many business financing options, but fortunately there are ways to improve your credit score (and your fundability). Aside from paying off existing debt, managing your debt utilization responsibly, and making future credit card payments on time, you can build your credit score with a credit card. It will take some time, but a strong credit score is worth the invested energy since it will open up many business loan options that would otherwise be out of reach.

3. Double-check all forms

While it may seem like a no-brainer to most business loan applicants, you’ll want to be absolutely sure that you research the required documents for each application that you fill out. Whether you fill a form incorrectly or forget to fill it out altogether, it only takes a minor mistake to disqualify your application for a loan. Double and triple-check that you’ve filled the application out in its entirety, and that all of the information you provide is accurate and up-to-date.

Important note: Applying for business financing through Become eliminates the need to fill out multiple applications for multiple lenders. With one fast and easy online application and dozens of top lenders to possibly qualify with, Become makes applying for business loans a breeze.

4. Maintain consistency with finances

Lenders will investigate your financial history, usually by looking back through your bank records. That will include your bank balance from month-to-month, your monthly revenue, monthly deposits, and so on. If those numbers fluctuate dramatically from one month to the next, it will be a signal to lenders that your business lacks stability (which adds to the risk the lender takes on).

Do your best to keep your bank balance, monthly revenue, monthly deposits – and really all of your bank activity – consistent. If you’re facing difficulties as a result of unpaid invoices piling up, you should develop strategies for dealing with non-paying customers.

Alternative finance options

The fact of the matter is that some financing options will be more difficult to qualify for than others. SBA loans, for example, offer some of the best terms and conditions for small business owners in need of financing. With competitive interest rates, low down payments, and the ability for poor credit scores to qualify, it’s understandable why getting approved for SBA loans is more difficult – because small business owners find them so desirable!

Another example of a funding solution that is generally more difficult to qualify for is an unsecured business loan. While they have the advantage of not requiring any collateral to be put up as security, in order to qualify for unsecured business loans you’ll need a strong credit score. Additionally, since lenders take on more of a risk in providing loans that aren’t backed by assets, they balance that risk by increasing interest rates. In short, the benefits offered by certain business loan types often come with a more demanding set of qualification criteria.

On the other hand, there are a number of business loan options that tend to be easier for small businesses to qualify for. Asset-based loans, compared to unsecured loans, have lower interest rates, lower credit score requirements, and have much lower down payments. Of course, the borrowing business owner will be placing his or her valuable assets at risk if payments aren’t made on time.

Of course, the type of business will affect the kind of industry loans a business needs, as well as the specific circumstances that business finds itself in. Be sure to weigh your options carefully in order to choose the right funding solution for your business.

The bottom line: Depending on your business’s specific financial situation, certain loan types may be better options than others. Always be sure to do your research before applying for small business financing.

Disclaimer: The information contained in this article is provided for informational purposes only, should not be construed as legal advice on any subject matter and should not be relied upon as such. The author accepts no responsibility for any consequences whatsoever arising from the use of such information.