Credit Score Soft Inquiry vs Hard Inquiry: What’s the Difference?

What’s the difference between hard and soft credit inquiries?

Hard and soft inquiries are types of credit checks that are often confused. Understanding the difference is important when it comes to credit management, and applying for funding or a form of credit. Here we’ll discuss the main differences between the two types of credit pulls.

Credit score soft inquiry vs hard inquiry:

When applying for credit or skimming over your credit report, you may have come across the terms ‘soft inquiry’ or ‘hard inquiry’ also known as ‘credit pulls’ and wondered what it all actually means.

Every time you apply for new credit, the ‘credit inquiries’ section of your report will change and affect your credit score. But does this occur with a hard inquiry, a soft inquiry or both? What’s the difference between the two and how do you conduct a credit inquiry removal? These are some of the questions we’re about to answer (and more).

But first, let’s go back to basics…

What is a soft credit check?

Soft inquiries (also known as soft pulls/credit pulls), occur when a company, institution or individual checks your credit as part of a wide background check and may even occur without your permission. Soft inquiries aren’t linked to any specific application for new credit and will only be visible to you.

Soft inquiries often happen without you even knowing it. Think about that credit card offer that just arrived in the mail – no company would waste their time or postage fees sending you the offer without first making sure you’re a suitable borrower. Surprisingly, even some employer background checks include soft inquiries on the applicant’s credit report. They want to make sure they’re hiring responsible individuals, after all.

When you check your own credit report (which is something you should do annually or even quarterly) this counts as a soft inquiry, as do loan or mortgage pre-approvals.

For example, when you apply for loan offers through Become, there’s no impact whatsoever on your credit score as only a soft pull is used.

A soft pull may occur due to:

- An employer checking your reliability

- Credit card issuer checking your credit to see if you qualify for their cards

- Brokers – to see if you will match with certain lender’s terms

- When you check your own credit report

- Lenders/insurance companies checking to pre-approve offers

Will a soft inquiry affect my credit score?

Because soft inquiries are only visible to you, they will in no way be considered as a factor in credit scoring models. In other words, no points will be shaved off your credit score, they are totally harmless and will NOT affect your score.

How to do a soft credit check:

If you’re wondering how to do a soft credit check yourself, you’ll need to request a free copy of your credit report from one of (or all three of) the three major credit bureaus; Equifax, Experian or TransUnion. You can get a free copy once a year. You will also be able to freely see your report within 60 days of being denied credit if your score is inaccurate, you’re unemployed or on welfare.

What is a hard credit check?

You’ll know about these because hard inquiries require your consent and happen when you actually apply for a specific credit option. When it comes to applying for credit, be it a mortgage, a credit card, a personal or business loan, the lender will check your credit report and score from one (or more) of the credit bureaus.

Will a hard inquiry affect my credit score?

A hard inquiry or ‘hard pull’ WILL affect your credit score and will not occur against your will, it is something that you will have to approve before it is conducted. Hard inquiries can shave as many as 5 points off of your FICO score and leave a lasting scar on your credit report for 2 years, so anyone else who does a soft or hard inquiry will see the inquiry.

Too many hard inquiries in a short time span can appear fishy to lenders. This is because opening many new credit accounts could mean you’re having issues paying bills or are at a higher risk of overspending. This is why hard inquiries have a negative effect on your credit score, but also why they will fade away relatively quickly.

On the other hand, having many hard inquiries in quick succession could also be the result of rate shopping – trying to find the best rate and deal available…

What if I’m rate shopping?

Fear not, credit scoring models understand that you may just be rate shopping and so all hard inquiries made within a 45-day period are counted as only one inquiry by FICO.

This is good news since each hard inquiry counts against your score, which really makes a difference if you have a borderline score. Even if your score is really good, you don’t want to make unnecessary inquiries that can reduce it.

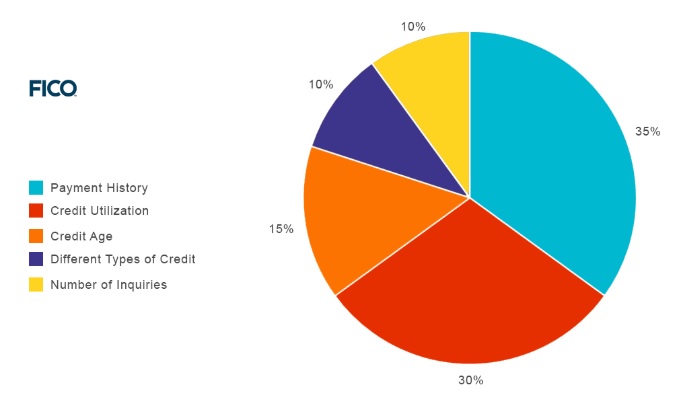

Just keep in mind that inquiries are only a tiny slice (10%) of the bigger pie when it comes to calculating your credit scores.

When calculating your credit score, the following components are taken into account:

Photo Ref: FICO

How to minimize the impact of hard credit inquiries

First, off, as you can see from the pie-chart image above, don’t sweat it too much – applying for new credit will only account for 10% of your FICO score which is pretty small. It’s something that has to happen in order to apply for new credit.

To minimize the impact of hard inquiries, it’s best to make all of your inquiries within a short period of time. So if you’re rate shipping, be sure to do it in a matter of weeks (keep it within 45 days maximum) rather than spreading it over months. This way, it will come up as one inquiry and have a smaller impact. Happy days!

How to remove inquiries from your credit report

When it comes to your credit report, inquiries are the least important component to be removed though if you wish, they can still be disputed and credit inquiry removal is possible in certain cases.

If you find a hard inquiry on your report that you don’t recognize or remember authorizing, you may have been a victim of identity theft – in this case, because it was conducted without your permission, you are permitted to dispute and remove it.

To dispute an inquiry and remove it, you’ll need to go directly to the creditor and send them a letter in the mail. Simply point out the inquiry, the issue and that you’d like it removed. You could also contact the credit bureaus where the inquiry was shown.

Read: How often should you check your credit score for more information on this.

Which loans you can qualify for with no hard credit inquiry?

When you apply for unsecured business loans (or any business loan) through Become, you’ll only incur a soft credit check – which will NOT harm your credit score. Become will then be able to show you which lenders you’ll be able to qualify with, essentially saving you from having to apply with each and every one and have them all conduct a hard credit check.

This way, you’ll be able to select your lender, knowing you can qualify already, and only then will the lender conduct a hard credit check. You’ll, therefore, be able to receive rates and terms that are most suitable for your business.

Hopefully now know all about the differences for credit score soft inquiry vs hard inquiry – if you have any questions, feel free to leave them in the comments below!