Construction Factoring

The 2019 Guide to finding the best construction factoring options

Time flies when you’ve got unpaid invoices. Days turn to weeks, weeks to months, and before you know it, you’re buried up to your hardhat in overdue bills.

The bad news: this is a common issue for small business owners in the construction industry.

The good news: there’s a solution that you can make good use of – construction invoice factoring.

Not familiar with the term? Keep reading and we’ll give you the long and short of what construction factoring is and how you can use it!

What is construction factoring?

Construction factoring (also referred to as construction invoice factoring) is a financial solution designed to help solve cash flow problems associated with unpaid invoices and non-paying customers in the construction industry. You can compare it with freight factoring, which serves the same purpose but specifically for the trucking industry.

Similarly to invoice factoring, the basis of construction factoring is that a lender provides roughly 80% of the money owed to you in the form of a lump-sum loan. The lender collects the payments from your customers and then pays you the remaining balance minus the fee for their services.

Unlike other types of business loans though, construction factoring can be difficult to acquire. The reason for that is (ironically) the same reason that construction companies seek factoring in the first place – unpaid construction invoices can take a while to collect.

This places construction companies in a bit of a ‘catch 22’ where the solution is often out of reach specifically because of the problem they’re looking to solve. It also creates something of a niche lending option, since fewer lenders are willing to provide construction invoice factoring.

That said, there are construction factoring companies out there that you can qualify with. We’ll get to that below.

What is construction factoring used for?

In the most fundamental sense, construction factoring is a business funding solution that’s used to free-up cash stuck in the form of unpaid invoices. That money can then be used to keep your business operating the way it should (or to improve it!).

You can use construction invoice factoring to:

- Hire more staff

- Pay employees

- Expand the business

- Purchase equipment

- Improve lead generation strategy

- Acquire raw materials and inventory

- Etc.

Aside from keeping your cash flowing smoothly, construction factoring will save you the time and stress of chasing down customers to pay. Construction factoring companies take on most of the risk since they’re providing you with the majority of the bills’ value upfront – which creates an incentive for them to do that chasing instead!

Side note: Developing a strategy to deal with non-paying customers is essential in the construction industry. It will likely be a recurring issue, and turning to construction invoice factoring too frequently can get expensive.

The best construction factoring companies of 2019

Though few in quantity, the construction factoring options available through Become are high in quality. The best part is that when you apply through Become, you gain access to a wide array of tools that will help improve your funding odds.

![]()

|

Qualifications |

|

|

Loan amount |

Up to $5 million |

|

Loan term |

Up to 12 months |

|

Payment schedule |

Weekly or monthly |

|

Rates |

Start at 4.80% |

|

Time in business |

Minimum 6 months |

|

Credit score (FICO) |

600 |

|

Collateral |

None |

Pros and cons of construction factoring

|

Pros |

Cons |

|

|

Are subcontractors eligible for factoring?

Yes, subcontractors are eligible for construction factoring.

As far as lenders are concerned, if your finances are healthy and you’ve demonstrated responsible borrowing habits, you should be able to qualify for construction invoice factoring whether you’re a subcontractor or a full-on construction company.

With that in mind, it’s important to remember that business loan eligibility criteria will involve a variety of factors including:

- Credit score

- Existing debt

- Monthly revenue

- Business age

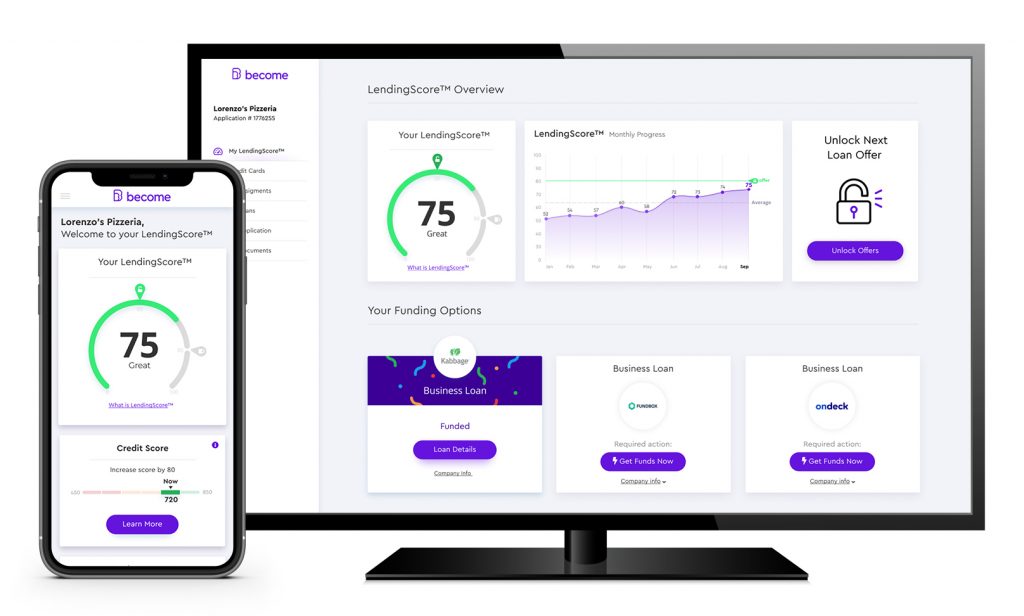

There are even more funding factors that impact your ability to obtain funding, so how are you to know which one is making the biggest difference?

Easy! The LendingScore™ technology designed and developed by Become analyzes your business’s financial profile and then gives you tailored insights into which funding factors have the largest impact on your fundability. Comparing alternative lending to bank lending is like comparing an electric car to a horse-and-buggy. Not only is it more comfortable, it’s also faster and more efficient!

[bctt tweet=”Comparing alternative lending to bank lending is like comparing an electric car to a horse-and-buggy. Not only is it more comfortable, it’s also faster and more efficient!” username=”Become_co”]

Those are just some of the ways that Become’s online business lending marketplace is revolutionizing the lending process through the power of fintech.

Invoice factoring vs invoice financing: What’s the difference?

The main difference between invoice factoring and invoice financing mainly comes down to who goes around to collect the payments due. With invoice factoring, the lender claims the responsibility of collecting the bills from customers. Invoice financing, on the other hand, leaves that responsibility with you, the business owner.

That’s not the only difference between invoice factoring and invoice financing though; you’ll also find that there are different fees as well as different amounts provided upfront.

For example, invoice factoring comes with an increased risk involved in chasing down the customers, which typically results in higher fees for invoice factoring (around 2%-4.5% monthly). Invoice financing tends to have lower fees since the business owner is still tasked with collecting payments (around 1%-3% monthly).

Similarly, the amount received upfront with invoiced factoring is usually a bit higher than with invoice financing, since invoice factoring entails the lender actually gaining ownership of the due invoices (while invoice financing leaves invoice ownership with your business).

Whether you go with invoice factoring or invoice financing, you’ll find that they are both among the fastest business loans available on the market. So if you’re in a tight financial position and you’ve got unpaid invoices sitting around, either one can serve as a quick fix to get you by.

When to use equipment financing instead

Construction invoice factoring isn’t always the best fit for every construction business or subcontractor. That’s precisely why there’s a variety of construction business loans available at disposal. Finding the right funding option for your business depends on several factors, including what you plan on using the funding for exactly.

Important note: Of course, the type of store you run will affect the kind of industry loans you, as well as the specific circumstances that you find yourself in. Weigh your options carefully in order to choose the right funding solution for your business.

Since the bulk of construction business operations rely so heavily on having the right equipment (and maintaining its proper functioning), it should come as no surprise that equipment financing is one of the most common funding solutions in the industry. If your main reason for seeking out construction factoring is to cover expenses related to purchasing or fixing equipment, then you should also strongly consider equipment financing.

Why should you consider lenders who provide equipment financing over construction factoring companies? First off, they don’t require any collateral since the equipment being financed serves as its own security. Secondly, you can get approved for up to 100% of the cost of the equipment, which can turn out to be significantly more than you’d get through construction factoring. The reasons go on, but the bottom line is that you should weigh your options carefully before choosing to go with a given type of business financing.

Build a better future

The construction industry has its fair share of obstacles, but acquiring funding doesn’t have to be one of them. If your clients are taking a long time to pay their bills, you can use construction factoring to give your business the cash boost it needs. But don’t forget – there are lots of kinds of construction financing solutions out there!

Become is here to help match you with the right lender and the loan type for your business. Apply today and start improving your funding odds with the power of financial technology!