How Our Customers Successfully Used Their First Business Loan

Whether you’ve just managed to score your very first business loan, or you’re in the process, you’re probably trying to figure out how you’re going to spend your business funds.

What Can a Business Loan Be Used For?

A business loan can be used in many, many ways. Whether you’re feeling giddy because you’ve planned out where every dollar is going to go or you’re feeling a touch overwhelmed and not so sure, it’s always useful to look to your peers. Have a look around and see how other business owners are spending their business funding. In this very special post, we’ll be detailing exactly how our customers here at Become, spend their very first business loan.

We’ll show you all the stats that we’ve managed to collect over the last year so that you can see how to use business loan and how other fellow business owners are using their funds – perhaps you’ll get a few ideas for yourself!

If you’re wondering ‘what can I use a business loan for’, you’re about to find out from real businesses how they used theirs. We’ll go over whether businesses are using the funds on capital expenditure, or revenue expenditure and help you make those critical business expense decisions.

What Is Capital Expenditure?

Capital expenditure, also known as ‘CapEx’ refers to the funds used by a business spent on purchasing or updating long-term assets. When we’re talking about long-term assets we are talking about those that are ‘fixed’ and usually physical assets. This could be in the form of equipment, vehicle or property (such as a warehouse or office space for example).

Capital expenditures are essentially major investments that provide great value in terms of generating income over a long time period. Companies will often use debt or equity financing to cover the substantial costs for expanding their business.

Capital expenditure decisions are critical to a business and should not be taken lightly. These fixed assets have a life of a year or more and due to their long-term effects, should be well-thought-out before taking action. Be sure to budget for these sorts of expenditures and carefully plan before throwing your money away.

What Is Revenue Expenditure?

Revenue expenditure differs to capital expenditure in that they are more short-term. Revenue expenditure includes the funds that you spend immediately. It could be in the form of expenditures that will help you to generate more revenue such as operational costs or perhaps just for the maintenance of existing assets.

Revenue expenditures are more of a recurring expense as opposed to one-off capital expenditures. Unlike capital expenditure, they can be fully tax-deducted in the same year as the expense.

How Businesses Spent Their First Business Loans:

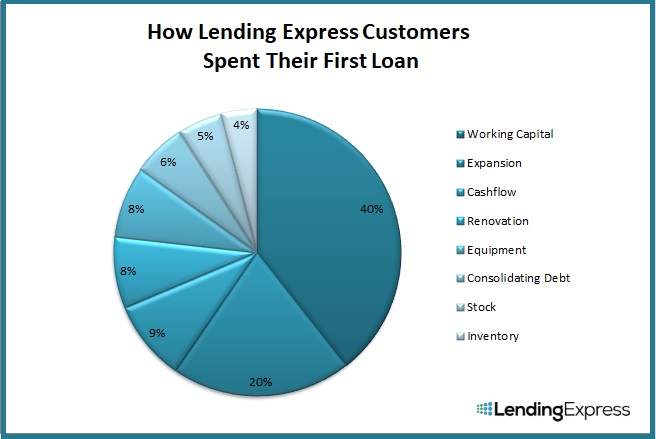

Now that you know the key differences between capital and revenue expenditure, let’s take a peep at the business owners that used Become to get their funding, and what they used their initial capital on (stats from full-year results of 2017):

As you can see, the majority (40%) of businesses spent their money on revenue expenditure, that is; working capital, helping to fund the everyday expenses of their business.

The second most popular category falls under ‘expansion’– which 20% of Become’s customers used their first loan for.

Cashflow: 9% of businesses used their funds to help even out their cash flow which highlights the importance of cash flow forecasting. Business owners often make the mistake of failing to spot that they are running low on cash and after all, it’s cash that makes the business go round. A U.S. Bank study by Jessie Hagan showed that 82% of businesses actually fail due to poor cash flow management. A business loan will help keep money flowing to allow for the usual operation of your business.

Renovation and Equipment: 9% of businesses used their funds for renovation and 8% on equipment with both categories falling under capital expenditure. This kind of business investment can work out beneficial for the long run. At Become, we have some lending partners specifically dedicated to business equipment loans which can take your business to the next level. Equipment financing pros and cons are far and spread so be sure to do your research beforehand.

Consolidating debt: 8% of businesses use their loan to consolidate debt. This is actually relatively low compared to the Federal Reserve’s Small Business Credit Survey (2017) which found that nearly a quarter of businesses applying for funding were seeking to refinance or consolidate existing debt.

It could be a wise idea to consolidate your loans in your business if you have a variety of different debts. Consolidating your existing business debts into one loan could actually have the benefit of lowering your interest rates and even reduce the size of monthly payments. They could also open the door for you to borrow additional working capital.

By having your loans consolidated into one, you’ll find it far easier to make repayments far and keep track of everything. Become has a few partners that offer this service.

Stock and inventory: together, stock and inventory accounted for 9%. Inventory and stock is the lifeblood of many small businesses. You may decide that this is necessary due to seasonal dips or to simply replenish stocks. To cover the costs for stock and inventory you could go for a term loan or line of credit.

- An unsecured loan has higher borrowing and longer repayment periods so this would be a better option for a one-time large purchase

- A line of credit offers more flexibility, it’ll act as a safety net and you can draw upon the funds whenever needed. With a line of credit, you’ll only ever pay back what you borrowed.

How to Choose What to Spend YOUR Business Capital On?

Off to the drawing board you go.

Now that you know what other businesses like yours spend their money on, you should have an idea of what area of your business needs that injection of funds the most. We suggest you take the time to sit down, forecast your cash flow and analyze those projections to see if they are in line with your overall business goals. This should give you a clear idea of which areas need the business funding the most or whether it might be a good idea to consolidate your debts.

When to use business loan:

Now you know what can a business loan be used for you may be wondering when to use a business loan? Timing isn’t everything. When it comes to taking out a business loan, if you have the right reason for getting the funds in the first place then the timing could be any time! The motivation is more important than the timing at the end of the day. It may be that you’re right at the start and need start up funds, you may be 6 months in and need more inventory, or you may be 5 years in and have cash flow issues or want to upscale your business.

How to Get a Small Business Loan

If you’re ready to take the next step for your business and don’t want to go through the banks’ long process (or perhaps are struggling to get funding from banks in the first place), there are plenty of alternative online lenders you can turn to.

Become has over 40 partners and when filling out an application, will take all of your details and needs and cross-analyze this with the lending partners. Become will then show you with your qualifications, which loans and terms you can qualify for. You then have the choice of whether to proceed with the lenders matched to you.

- You can get your funding in as little as 3 hours!

- Short online application form

- No hard credit check (credit score will not be affected

- Obligation free

- No need for face-to-face meeting (times are changing!)

Feel free to contact support@become.co with any questions you may have!